The funding fee is the first mechanism for Bitcoin perpetual futures, designed to maintain the contract worth as shut as doable to the spot worth of BTC. It’s a periodic cost trade between lengthy and brief merchants, decided by the distinction between the perpetual futures and spot costs. When the funding fee is constructive, lengthy positions pay shorts, and when it’s unfavourable, shorts pay longs.

Monitoring the funding fee is essential in analyzing the markets because it is among the greatest indicators of dealer positioning, particularly in a leveraged buying and selling setting. When the funding fee is persistently excessive or constructive, it signifies bullish sentiment as extra merchants are prepared to pay a premium to carry lengthy positions in perpetual contracts. Conversely, when the funding fee is unfavourable, it signifies bearish sentiment and merchants are extra inclined to brief the asset and pay a premium.

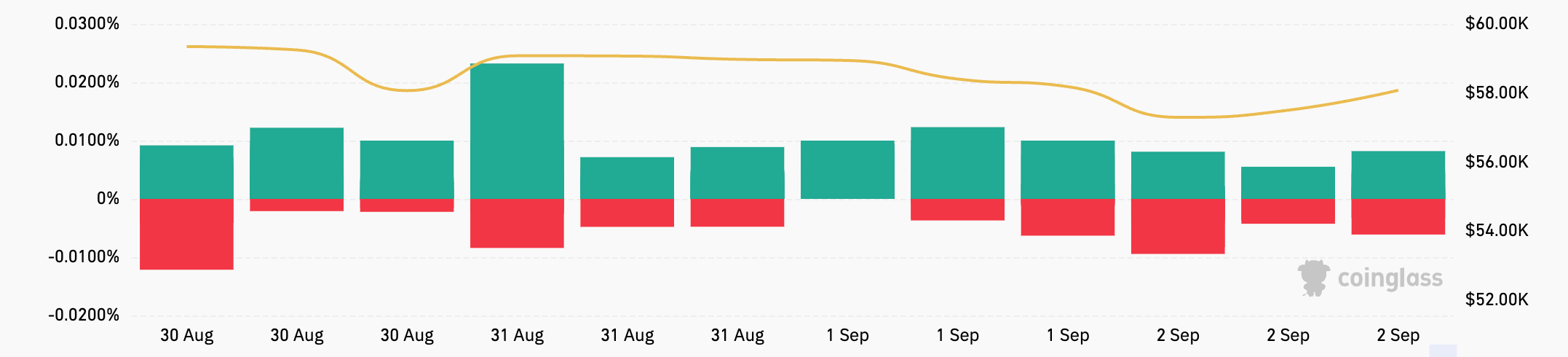

All through the weekend, funding charges for USDT and USD-collateralized contracts fluctuated throughout exchanges. On August 31, funding charges had been principally constructive, indicating bullish sentiment, however of various magnitude. The best funding fee was on Bitmex at 0.0089%, whereas the bottom was on OKX at 0.0029%. On September 1, notable modifications had been seen particularly on Binance and Bybit, which had been unfavourable at -0.0004% and -0.0009%, respectively, indicating a rise in bearish sentiment on these exchanges.

This pattern continued on September 2nd and was extra pronounced on Bybit and OKX, with each platforms recording unfavourable funding charges of -0.0040%, indicating rising strain from brief positions. In distinction, Bitmex, which recorded the best funding fee on August thirty first, remained constructive, though it dropped considerably to 0.0048% by September 2nd. HTX's funding fee additionally dropped, however remained constructive at 0.0014%. The big variations in funding charges between exchanges are on account of variations in dealer sentiment and positioning on every platform, that are doubtless influenced by liquidity, buying and selling quantity, and the precise dealer base.

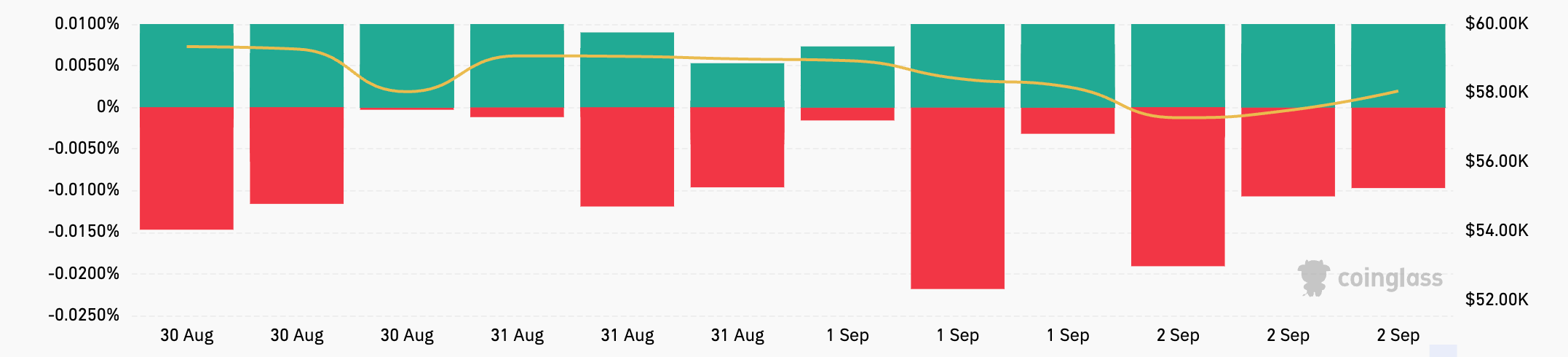

Funding charges for token margin contracts over the identical interval diversified broadly. By September 1, most exchanges' funding charges had turned unfavourable, with Bybit and OKX dropping to -0.0096% and -0.0044%, respectively. The divergence grew to become much more pronounced on September 2, when Bybit's fee dropped to -0.0191%, signaling sturdy bearish strain. In the meantime, HTX noticed a major improve to 0.0100%, signaling a pointy reversal of sentiment on that platform.

This distinction in funding charges between the USDT/USD margin contract and the token margin contract exhibits how merchants in these markets behave in another way.

Stablecoin and fiat-settled USDT and USD margin contracts are generally most popular by merchants who don’t wish to be uncovered to Bitcoin worth fluctuations when settling their income and losses. These contracts are standard amongst retail merchants and merchants who use leverage to make directional bets on Bitcoin worth actions with out affecting their underlying Bitcoin holdings.

However, token margin contracts are settled in BTC or different cryptocurrencies, making them extra enticing to merchants with a long-term bullish view on Bitcoin and people who can tolerate the inherent danger of further volatility. These contracts are sometimes utilized by extra subtle merchants and people with a long-term holding technique, as their publicity to Bitcoin worth may end up in larger income in addition to larger danger.

The distinction in funding charges between these two varieties of contracts over this era signifies completely different danger tolerances and techniques of merchants. The unfavourable funding charges for Token Margin contracts point out that merchants in these markets had been extra bearish or danger averse and anticipated additional declines in Bitcoin costs.

In distinction, funding charges for USDT/USD margin contracts have typically remained secure and constructive, suggesting that merchants in these markets are extra bullish or much less involved about short-term worth fluctuations.

It is usually necessary to research these modifications in funding charges together with Bitcoin worth actions. Over the weekend, Bitcoin's worth fell from $58,970 to $57,570, a comparatively modest decline given Bitcoin's historic volatility. Nevertheless, the sudden fluctuations in funding charges, notably the unfavourable shifts in Binance and Bybit's USDT/USD margin contracts and the intense negatives in token margin contracts, recommend that merchants are positioning for the chance of additional declines.

The general decline within the volume-weighted funding fee from 0.0050% on August thirty first to -0.0017% on September 2nd exhibits how sudden this transformation in sentiment was, as merchants elevated their brief positions or diminished their publicity to lengthy positions.

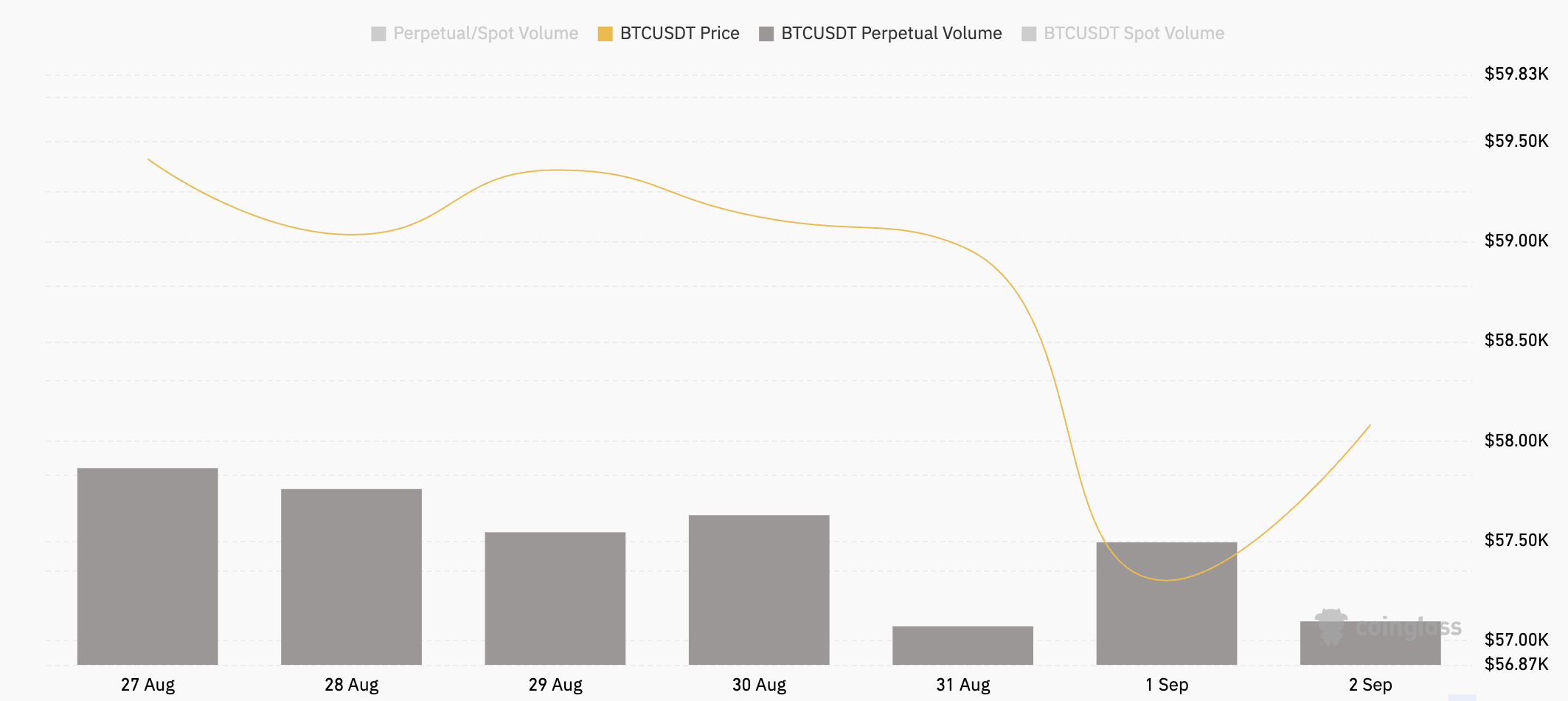

Perpetual futures buying and selling volumes additionally fluctuated broadly over the weekend, with sharp declines on August 31 and September 2, adopted by a rise in buying and selling quantity on September 1. This means that merchants had been both taking income or reducing losses amid market uncertainty, resulting in a lower in OI and buying and selling exercise as funding charges started to fluctuate.

The publish Fluctuations in Bitcoin Funding Charges Sign Market-wide Warning appeared first on currencyjournals

{kind=link}